https://www.adb.org/outlook/editions/july-2024

Interest rates in the United States and other advanced economies continue to shape the outlook, which is subject to several downside risks. Uncertainty on the United States election outcome, elevated geopolitical tensions and trade fragmentation, property market fragility in the People’s Republic of China, and weather-related events could hurt growth. Meanwhile, La Niña is an upside risk due to expected higher rainfall and cooler temperatures.

Caucasus and Central Asia

The Caucasus and Central Asia growth forecast is revised up to 4.5% from 4.3% in 2024 and 5.1% from 5.0% in 2025, driven by stronger-than-expected growth in Azerbaijan and the Kyrgyz Republic. Azerbaijan’s economy expanded by 4.3% in January to April 2024, driven by transport and construction aided by public spending. The Kyrgyz Republic’s growth rate is estimated to have been 8.8% in Q1 2024 due to strong output in services and construction funded by domestic and foreign investment. Economic activity in other subregional economies has been similarly robust. Armenia grew by 9.2% in Q1 2024, led by growth in manufacturing. Georgia’s economy expanded by 9.0% in the first 4 months of 2024, as strong credit supported both domestic consumption and investment. Partly due to a sharp rise in exports, including gold sales, Tajikistan continued its strong growth, at the rate of 8.2% in Q1 2024. Growth in Turkmenistan is driven by public investment and net gas exports. A surge in fixed capital investment in Uzbekistan led to 6.2% growth in Q1 2024.

Inflation forecasts for 2024 and 2025 in the Caucasus and Central Asia are revised down. The revised forecast mostly reflects lower-than-expected price levels observed in Armenia, Georgia, and the Kyrgyz Republic. In Armenia, a strong local currency, among other factors, brought a 0.8% deflation in the first 5 months of 2024, a substantial decline from the 5.2% inflation in the same period of 2023. Amid currency appreciation, Georgia’s inflation for the first 5 months of 2024 was also limited to 0.9%. In the Kyrgyz Republic, inflation dropped to 4.6% in May 2024, primarily reflecting price movements of major commodities, from 11.3% a year ago. Inflationary pressures are also subsiding in other economies of the subregion. In January to May 2024, Kazakhstan’s inflation rate slowed to 9.0%, down from 18.5% in the same period in 2023, due to a stable exchange rate and relatively tight monetary policy. Tajikistan’s inflation was 3.8% in the first 4 months of 2024. In Uzbekistan, inflation decelerated to 9.2% in the first 5 months of 2024 from 11.4% a year earlier.

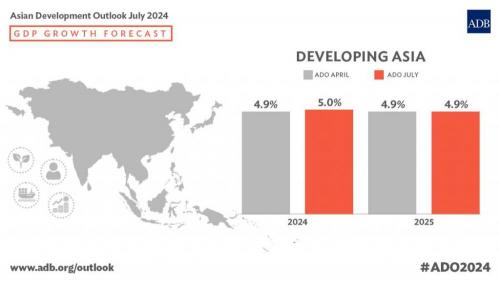

East Asia

The 2024 growth outlook for East Asia has been revised slightly up to 4.6%, remaining at 4.2% for 2025. The upward adjustments in 2024 forecasts for the Republic of Korea (ROK) and Taipei,China, due to strong exports of semiconductors and AI goods, led to a slight rise in the subregional average. GDP projections for the People's Republic of China (PRC) are unchanged, supported by a recovery in services consumption and robust exports, which counterbalances the continued property market downturn.

The inflation forecast for East Asia is adjusted down to 0.8% in 2024, remaining at 1.6% in 2025. In the PRC, consumer price inflation averaged 0.1% in the first 5 months of 2024, down from 0.8% a year earlier. Nonfood inflation increased to 0.8% from 0.4% a year ago, driven by higher service prices. Food prices fell by an average 2.8%, with pork prices down 2.7%. Lower inflation has led to a downward adjustment in the 2024 forecast, while the 2025 forecast remains unchanged at 1.5%, given ongoing policy stimulus to boost domestic demand and help the property market recover. Inflation forecasts for other East Asian economies remain unchanged and on target.

South Asia

South Asia is on course to largely achieve ADO April 2024 growth forecasts. Downward revisions for GDP growth in Bangladesh and Maldives over the forecast period are offset in 2024 by upward revisions for Bhutan, Nepal, and Pakistan, leaving the region’s 2024 growth forecast unchanged at 6.3%. The growth forecast for 2025 is revised down marginally to 6.5%. In Bangladesh, the lower growth forecasts for fiscal year 2024 (FY2024, ending 30 June 2024) and FY2025 come mainly from downward revisions to growth in industry. Dampened performance of the construction sector is the main reason for lower growth forecasts for Maldives in 2024 and 2025, with lower-than-expected growth in the fisheries sector this year also contributing. Bhutan’s GDP growth forecast for 2024 is adjusted upward due to a greater-than-expected increase in the government budget for FY2024 (ended 30 June 2024) and better tourism prospects. Nepal’s GDP projection for FY2024 (ending mid-July 2024) is also revised up due to higher-than-expected growth in agriculture and services. The provisional government estimate of GDP growth in Pakistan for FY2024 (ending 30 June 2024) stood at 2.4%, reflecting robust agricultural output due to improved weather conditions and subsidized government credit, among other factors. Although the economic performance in Q1 2024 in Sri Lanka exceeded ADO April 2024 expectations, growth forecasts for 2024 and 2025 are retained as there remain uncertainties as the election cycle begins in the latter half of the year. While Afghanistan’s economy is showing signs of recovery, the weak investment climate, tight fiscal space, and waning international humanitarian and basic needs support underlines its fragility.

The inflation forecasts for South Asia are nudged up to 7.1% in 2024 and maintained at 5.8% in 2025. Although inflation forecasts of Bhutan, India, and Pakistan for FY2024 and FY2025 remain the same as in ADO April 2024, the inflation projections for Bangladesh and Maldives are now expected to be higher. Despite several measures to curb inflation, monthly inflation rates in Bangladesh continued to be near double digits in the first 11 months of FY2024 and may persist due to high domestic food prices. Inflation in Maldives is forecast to be higher due to the shift to targeted subsidies instead of a broader set of subsidies. In contrast, the inflation forecast in Sri Lanka for 2024 is revised down as supply-side conditions improved alongside better external buffers and the availability of foreign currency. In Nepal, average inflation moderated to 5.8% in the first 10 months of FY2024, prompting a downward adjustment in the FY2024 forecast. Inflation is also revised down in FY2025 as transport-related prices should moderate further.

Southeast Asia

Growth forecasts for Southeast Asia remain at 4.6% in 2024 and 4.7% in 2025 on solid improvement in both domestic and external demand. Consumption—fueled in part by stable prices and increasing tourism-related activities—continued to lift Southeast Asian economies, though tempered a bit by the tight monetary environment. Higher spending on infrastructure projects in the subregion’s big economies continue to boost investment demand and growth. The expected export recovery is also fueling growth with manufacturing purchasing managers’ indexes remaining positive for major exporting economies, signaling increasing production. Except for the Lao PDR, growth forecasts are unchanged for all economies in 2024 and 2025.

ADO April 2024 inflation forecasts for Southeast Asia are retained for 2024 and 2025. In 2024, inflation fell in most economies as global food prices eased despite oil price volatility. Thailand’s inflation forecast for this year was reduced from 1.0% to 0.7% as the average inflation for the first 5 months was below ADO April 2024 expectations. Prices of meat, fish, pork, short mackerel, sea bass, and fresh vegetables were lower than expected due to large market supply. For 2025, inflation is adjusted down from 1.5% to 1.3%. The inflation forecast was raised for Myanmar this year due to the pass-through effects from currency depreciations and the Lao PDR next year with core inflation rising steadily and expectations having set in. Except for the surprise rate hike by Bank Indonesia in April, monetary authorities have delayed policy rate cuts to keep local currencies competitive against the US dollar. The Indonesian rupiah, Philippine peso, Thailand baht, and Vietnamese dong all depreciated since the start of the year as investors moved to safe assets such as gold and the US dollar.

The Pacific

Growth forecasts for the Pacific remain at 3.3% in 2024 and 4.0% in 2025. Robust international arrivals and the resumption of public infrastructure projects continue to drive the growth outlook, along with revived mining activity in Papua New Guinea, the subregion’s largest economy. However, the unchanged subregional average does not reflect the downward revision in Vanuatu’s forecast arising from the May 2024 liquidation of Air Vanuatu, the national carrier, which had an immediate impact on tourism and will likely have fiscal implications as well. The projections for Solomon Islands are adjusted upward because data updates indicate the economy has been performing more strongly than earlier estimated.

Inflation in the Pacific remains unchanged and forecast to rise to 4.3% in 2024 and 4.1% in 2025. The subregional averages are driven by higher inflation expected in Papua New Guinea and Fiji, the subregion’s largest economies. However, they mask upward revisions in the 2024 projection for the Cook Islands and the 2024–2025 projections for the Marshall Islands. Both changes result from data updates that show inflation, driven largely by increases in food prices, has been higher than previously estimated.